For therapy seekers, sometimes accessing an in-network therapist through your plan can be challenging. For therapists, you want to make the payment process as seamless as possible so your clients can receive care and be properly reimbursed. That’s where superbills come in. This option allows clients to use their mental health care insurance benefits and get reimbursed without needing to find an in-network provider.

Whether you’re using superbills as a provider or patient, knowing how they work is essential in reducing out-of-pocket care costs and making the process faster and easier. This is especially important as self-pay and out-of-network therapy are on the rise.

Below, we explain therapy superbills and how to prepare them for a smoother reimbursement process.

What Are Therapy Superbills?

Therapy superbills are itemized receipts of services provided by a mental health professional. They usually come as a PDF or a one-page receipt that the therapist generates for clients. Insurance companies need a superbill from the patient so they can get reimbursed for services using their insurance benefits.

A superbill typically includes specific information, such as the date and time of the therapy session, the client’s and the provider’s identifying information, procedures, diagnostic codes and fees the client paid for the service. Including all of this information can ensure the insurance provider accepts the superbill and reimburses the client.

When and Why Are Superbills Used?

Superbills are often used by out-of-network providers and clients with therapists who do not accept their specific insurance. They might also be used by clients who need therapy in a niche area not widely covered by in-network providers. Superbills allow clients to access more providers, helping them get the care they need without dealing with the complexities of insurance.

Therapists must use superbills to ensure clients can access their care, and use insurance benefits to reduce out-of-pocket costs. They can reduce a therapist’s administrative workload by helping them avoid complex insurance billing and payment delays. That way, they can focus solely on providing therapy to clients.

What to Include on a Superbill

To make sure insurance companies accept a superbill, providers will need to include specific information on it, like:

- The client’s full name, date of birth and address.

- The therapist’s full name, professional credentials, national provider identifier (NPI), license number and practice contact information.

- Service details like the dates of each session, descriptions of the services and diagnostic codes.

- The cost of each service and the total amount the client paid.

Additionally, providers might also need to include supporting documentation, like a claim form, invoice or detailed therapy notes, if requested, to make sure clients receive reimbursement.

How to Prepare a Therapy Superbill

The superbill and out-of-network insurance process usually follows these steps:

1. Understand Out-of-Network Benefits

If you know you will be using a superbill for your therapy, begin by asking about your insurance policy’s out-of-network coverage. For example, you or your therapist should contact your insurance provider about:

- The percentage of costs covered.

- Whether you need to meet an out-of-network deductible.

- How reimbursement will be calculated, such as a percentage of the billed rate or a set fee.

- How the claim submission process works, and if they need any documentation from you.

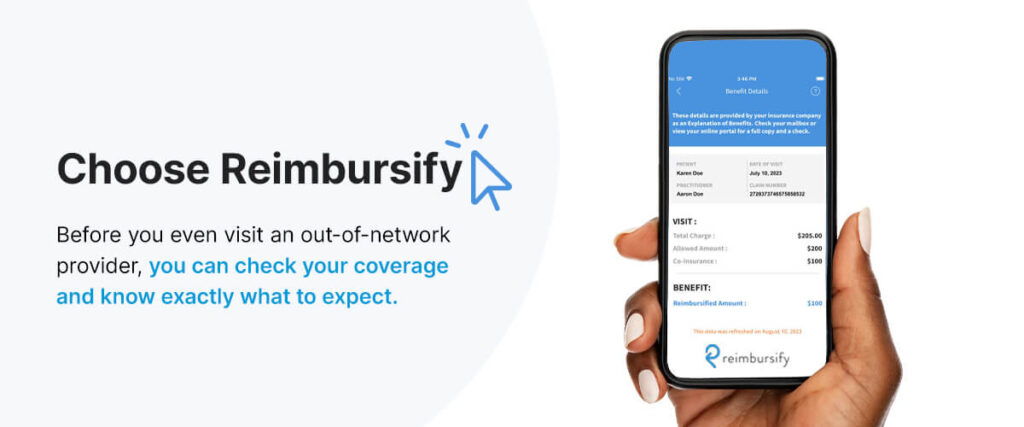

A digital insurance claims management system can make this process easier by instantly verifying your benefits. Before you even visit an out-of-network provider, you can check your coverage and know exactly what to expect for your reimbursement, eliminating surprises later on.

2. Receive and Review the Superbill

After your therapy appointment, ask your provider for a superbill. Make sure the superbill includes all necessary information, like your full name, insurance ID number, the provider’s information, when services occurred and types of treatments that were rendered. It should also clearly list service and diagnostic codes and the total amount paid.

3. Complete Any Necessary Claim Forms

Next, ask your insurance company if they need you to submit a specific claim form along with the superbill. Make sure you complete the claim form accurately so that it aligns with your superbill.

4. Submit the Claim

Ask how your insurer wants you to submit your claim form and superbill. Some options could include an online submission, mailing the documents or faxing them. In some cases, you can easily prepare and file your claim through a digital platform, streamlining the process. Make copies of everything you submit so you have it for your personal records.

5. Track the Claim and Follow Up

After submitting the claim, follow up with your insurance company to make sure they’ve received it and ask about its status. If denied, you’ll want to review the explanation of benefits (EOB) for a reason and explore ways to resubmit or appeal the decision.

Some platforms let you track your claim after submitting it while handling the back-and-forth and follow-up process with insurance to help you avoid denials.

6. Receive Reimbursement

If your claim is approved, you’ll get reimbursed through your plan’s benefits. Make sure you look at your EOB to see what was covered and the amount of your reimbursement.

Superbill vs. Direct Insurance Billing

You’ll want to decide when to use a superbill and when to bill directly through insurance. Each has its own pros and cons, depending on the case. Choose superbills if you want provider flexibility, but choose direct billing for convenience if your provider is in-network.

When to Use Superbills

Superbills are suited for cases where the therapist is out-of-network or doesn’t bill insurance directly. They can reduce the therapist’s administrative workload, give them more control over their rates, and allow them to grow a wider client base. For clients, superbills can grant them more flexibility in choosing therapists and allow them to receive reimbursement even if the therapist is out of network.

When to Bill Insurance Directly

Direct insurance billing is often used when the therapist is in-network and already bills the insurance company directly. It can mean less paperwork for the client, but it is limited to only in-network providers.

If you want the flexibility of choosing your therapist and a streamlined reimbursement process, using superbills with a tool like Reimbursify can be the best of both worlds — easy for therapists, empowering for clients.

Reimbursify Makes Therapy Superbills Easy

Superbills can be beneficial for patients and providers alike. They allow clients to focus on their health rather than the complexities of insurance while improving financial outcomes for out-of-network providers. However, superbills can be confusing and tough to prepare without professional help. At Reimbursify, we make it easier than ever to generate, submit and track superbills. Our insurance claims platform lets patients and providers submit claims and superbills easily and accurately, helping to avoid errors and maximize reimbursements.

Manage reimbursements all in one place, file claims on behalf of your clients and enjoy easy claim filing. Appreciate a quick, straightforward and entirely paperless claims and superbill-filing process with Reimbursify.

If you are a therapy client, you can download our app to get started. If you are a practitioner, sign up for a plan today.