Navigating insurance can feel overwhelming, especially when you are paying out of pocket for care you need and are unsure if you’ll be reimbursed. Whether you’re a patient seeing a trusted therapist who isn’t in-network or a practitioner trying to help your clients understand their benefits, the process can seem confusing, time-consuming and frustrating.

The good news is that you don’t have to figure it all out alone. This guide breaks down how out-of-network insurance reimbursement works, so you can walk away with clarity, confidence and practical tools to help you get reimbursed faster and with less stress.

What Is Out-Of-Network Care?

When a health care provider doesn’t have a contract with your insurance company, they’re considered “out-of-network.” This doesn’t mean you can’t see them. It means your insurance plan may cover a smaller portion of the cost, or none at all, depending on your benefits.

Why It Happens

Patients may choose out-of-network providers because:

- They want access to a specialist who isn’t in-network.

- The nearest in-network provider has a long waitlist.

- The quality or type of care they’re seeking isn’t available in-network.

What It Means for Patients and Employers

For patients, out-of-network care usually means paying the provider up front and then submitting a claim to the insurance company for reimbursement. For employers offering health benefits, it can mean encouraging employees to understand their out-of-network options, especially when it comes to supporting access to quality care.

Does Your Insurance Cover Out-Of-Network Services?

It depends on your plan. Many Preferred Provider Organization (PPO) plans include out-of-network coverage, though at a lower reimbursement rate. Health Maintenance Organization (HMO) plans, on the other hand, often don’t.

That’s why verifying your benefits before booking care is essential. Some providers even use tools like Reimbursify to check your insurance and show you an estimate of what percentage you may be reimbursed before your visit.

How to Get Reimbursed From Out-Of-Network Insurance Claims

The claims process takes a bit of organization and awareness. Out-of-network insurance reimbursement steps usually include:

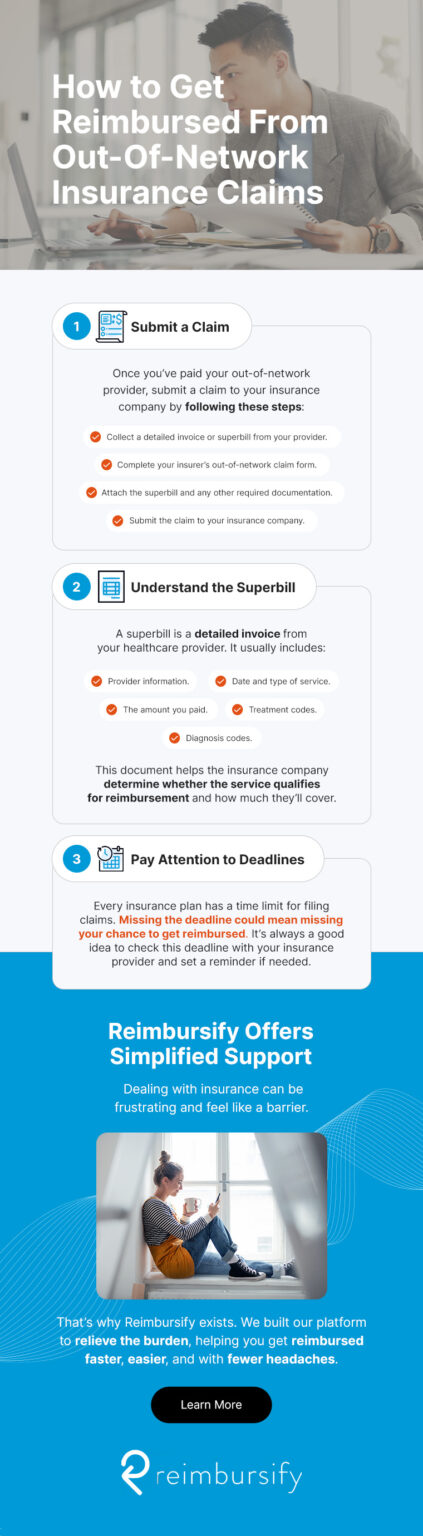

1. Submit a Claim

Once you’ve paid your out-of-network provider, you’ll need to submit a claim to your insurance company. The submission process typically includes the following steps:

- Collect a detailed invoice or superbill from your provider.

- Complete your insurer’s out-of-network claim form.

- Attach the superbill and any other required documentation.

- Submit the claim to your insurance company.

2. Understand the Superbill

A superbill is a detailed invoice from your health care provider. It usually includes:

- Provider information.

- Date and type of service.

- The amount you paid.

- Treatment codes.

- Diagnosis codes.

This document helps the insurance company determine whether the service qualifies for reimbursement and how much they’ll cover.

3. Pay Attention to Deadlines

Every insurance plan has a time limit for filing claims. Missing the deadline could mean missing your chance to get reimbursed. It’s always a good idea to check this deadline with your insurance provider and set a reminder if needed.

How Different Types of Care Impact the Reimbursement Process

While the reimbursement process is relatively standard, there can be slight differences depending on the type of care. For example:

- Mental health services may require additional documentation or treatment codes.

- Physical therapy might have stricter pre-authorization requirements.

- Nutritional counseling or alternative therapies may only be covered under specific conditions.

Each insurer and plan may treat these services differently. When in doubt, check your benefits or ask your provider to verify them.

Key Tips for a Smooth Reimbursement Experience

Being prepared before and after your appointment makes a big difference in how smoothly your reimbursement process goes:

- Verify benefits in advance: Know your out-of-network deductible and reimbursement rates before you book care.

- Keep copies of everything: Save your receipts, claim submissions and any communication with your insurer.

- Request a detailed superbill: Make sure it includes all the required fields and codes.

- Follow up: Don’t hesitate to call your insurance company if your claim is delayed or denied.

Common Missteps to Avoid

Preparation involves understanding a few common stumbling blocks that may complicate your reimbursement process:

- Submitting claims after the deadline

- Assuming your care will be reimbursed without checking your plan details

- Missing required codes or information on the superbill

How Reimbursify Simplifies Out-Of-Network Claims

The above information details what to expect with out-of-network reimbursement. It may involve hours of paperwork or endless back-and-forth with your insurer. Reimbursify makes the entire process easier.

Use these three steps to stay on track and feel in control of your health care and insurance coverage like a pro:

- Download the app and submit your claim: Download the Reimbursify app from the App Store or Google Play. Once you’re ready to submit a claim, complete some basic information about your visit, such as patient name, date, practitioner, diagnosis and service code from your superbill, and submit.

- Track your claim status: Review your claim status at any time from your Claims dashboard.

- Get reimbursed quickly: Approved claims are paid directly to you by your insurance company.

Graphic to include: https://webpagefx.mangoapps.com/msc/MjM5MjE0MV8xNTE4ODc2MA

Reimbursify Makes Out-Of-Network Reimbursement More Streamlined

Reimbursify is packed with features designed to make claiming out-of-network reimbursements quicker and easier for patients and health care practitioners.

Our system provides:

- Simplified claims process: Submit claims from your mobile device in a few minutes.

- Secure, HIPAA-compliant platform: Maintain patient confidentiality, ensuring strict privacy of sensitive health information.

- Real-time claim tracking and faster payments: Stay in control and track your claims throughout the process.

- Interactions with insurance companies: Save time and let Reimbursify follow up with your insurance company.

- Dedicated customer care: Find support every step of the way with a team experienced in navigating the complexities of out-of-network reimbursements.

Frequently Asked Questions

Get your pressing questions about Reimbursify answered.

1. How Long Does It Take to Get Reimbursed?

You stay in complete control and can track the progress of your claim on the app throughout the process. Reimbursements using Reimbursify are typically received within a few weeks.

2. What Types of Services Are Eligible for Reimbursement?

The app facilitates a wide range of health care specialties and services, from speech and physical therapists to fertility specialists and lactation services. Reimbursify also supports claims for appointments with many specialized mental health service providers.

3. Can I Submit Multiple Claims?

Yes, each out-of-network claim is unique and can be tracked separately on the app dashboard. Claims for visits to the same practitioner over several visits with the same information can even be cloned to further speed up the claim submission process.

Reimbursify Offers Simplified Support

Dealing with insurance can be frustrating and feel like a barrier between you and the care you need. Whether you’re a patient trying to get reimbursed for a therapy session or a provider trying to help your clients afford the services they rely on, the system can get complicated.

That’s why Reimbursify exists. We built our platform to relieve the burden so you can get reimbursed faster, easier and with fewer headaches. Reach out for more information, or download the app for free now!